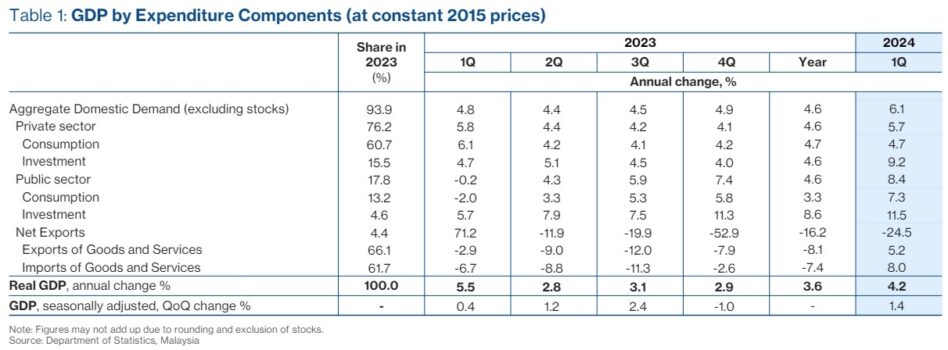

THE Malaysian economy got off to a cautiously decent start this year. It is heartening to have the economy growing at a relatively healthy pace of 4.2% year-on-year (yoy) in 1Q 2024 after the growth momentum having tapered 2.8% to 3.1% between 2Q and 4Q 2023.

This was in line with our estimate (4.3%) but beating market expectations (3.9%). The higher GDP growth was supported by continued growth in domestic demand and a smaller drag from exports.

Nevertheless, it remains a challenge to sustain higher GDP growth in the remaining quarters of 2024 as the headwinds and tailwinds are roughly balanced. We maintain this year’s GDP estimate at 4.5% (2023: 3.6%; 2022: 8.9%) with growth averaging +4.3% in 1H 2024 before strengthening to between 4.6% and 4.8% in 2H 2024.

Buoyed by positive sentiments in global equity markets and in anticipation of better economic and corporate earnings prospects, the local market capitalisation hit a record high of RM2 tril with the benchmark index FTSE Bursa Malaysia KLCI (FBM KLCI) surpassing 1,600 points for the first time in two years.

Besides the buying support of local institutional funds, foreign institutional investors have shown some buying interest albeit not on a broad-based sector basis. The market and investors are encouraged by a slew of investment announcements (approvals, committed and prospective) in 2022-2023 and up to 1Q 2024.

Detailed scenario

Consumer spending grew by 4.7% yoy in 1Q 2024 (4Q 2023: 4.2%) despite being dented by inflation and rising cost of living.

There was lower spending on food and beverages (1Q 2024: 4.0%; 4Q 2023: 5.9%), transport and communication as well as recreation services. Higher spending was seen on housing, water, electricity, furnishings, household equipment, routine household maintenance, and restaurants and hotels.

While we expect cautious consumer spending this year, households on aggregate are still benefiting from a few factors that together should remain supportive of spending in the remaining quarters of 2024 and 2025.

These are spending and income relief from the Employees Provident Fund’s (EPF) Flexible Account 3; additional cash handout accompanying the anticipated roll-out of targeted fuel subsidy rationalisation in 2H 2024; and more than 13% salary hike for 1.7 million civil servants.

Still, households are likely to become more cautious toward spending in anticipation of the implementation of fuel subsidy rationalisation that could increase inflation and cost of living.

Investment dynamics are underpinning the economic growth. Total gross fixed capital formation comprising public and private investment expanded strongly by 11.5% and 9.2% in 1Q 2024 respectively (11.3% and 4.0% in 4Q 2023 respectively), a positive sign to underpin the contribution of domestic demand.

Private investment is securing strong growth amid facing the headwinds of high business operating costs, including raw materials, logistic cost and impact of the weakening ringgit. Private investment expanded higher by 9.2% in 1Q 2024 (4.0% in 4Q 2023) with contribution coming from the manufacturing, services and oil & gas (O&G) sectors.

Private investment boom

We believe the country is at the beginning of a boom in private investment, supported by the on-going progress of multi-year projects and massive investment approvals totalling RM906.6 bil in 2021-2023, of which the manufacturing sector garnered the largest amount of RM431.3 bil or 47.6% share of total.

This is followed by services (RM422.5 bil or 46.6%) and primary sector (RM52.8 bil or 5.8% share). More than 85% of the manufacturing projects approved from 2021 to 2023 have been implemented to date.

By anchoring on a clear set of national economic growth and investment priorities such as the National Investment Aspirations, the Madani Economy framework, the New Industrial Master Plan (NIMP) 2030, the National Energy Transition Roadmap (NETR) and the Malaysia Artificial Intelligence Plan (2021-2025), private expansion is poised to spur expansion of both the domestic direct investment (DDI) and foreign direct investment (FDI).

Given the tetanic shifts in global geoeconomic landscape, it is critical to ensure that Malaysia remains a competitive destination for global/regional investors and manufacturers seeking more resilient and conflict-free supply chains who wish to diversify their operations and additional lines to China under the China Plus One strategy.

The government must execute well to implement structural reforms, enhance investors and businesses confidence, facilitate investment as well as ensuring policy transparency and consistency, cutting down wastage and red tapes, and weeding out corruption and kickbacks.

This would raise business efficiency of private sector as well as enhance a favourable investment climate which will ultimately serve as a strong catalyst to lift higher private investment and economic growth.

Beware of inflation

All economic sectors have registered positive growth in 1Q 2024. The top performer was 11.9% growth in the construction sector (4Q 2023: 3.6%) on a faster implementation of infrastructure projects.

We expect the sector to remain strong in the near-to medium-term given the on-going and new civil engineering projects such as Penang LRT, airports expansion, building and upgrading of roads and bridges, and the re-instatement of LRT stations in Klang Valley.

The services sector which expanded by 4.7% in 1Q 2024 (4Q 2023: 4.1%) will continue to sustain higher growth in the quarters ahead, thanks to stronger revival in trade, continued consumer spending and higher tourists’ arrival.

The manufacturing sector which turned around to record +1.9% growth in 1Q 2024 from a marginal decline of 0.3% in 4Q 2023 is expected to gain stronger growth traction in the remaining months backed by firmer rebound in demand of electronics and electrical (E&E) products, transport equipment, food processing and construction-related building materials.

Will inflation surprise on the upside in 2H 2024? Bank Negara Malaysia (BNM) expects headline and core inflation to average between 2.0%-3.5% and 2.0%-3.0% for the year respectively after incorporating the potential impact of fuel subsidy rationalisation.

We caution that going into 2H 2024 and beyond, the inflation trajectory may subject to upside risk due to the potential fuel subsidy rationalisation, the EPF Flexible Account withdrawal and the proposed pay hike for public civil servants.

Should there be any demand-pull price pressures, BNM may have to reassess the stance of its monetary policy going into 2025.

The central bank’s priority now is to sustain steady economic growth while keeping close vigilant on inflation risks. We expect BNM to hold the interest rate steady at 3.0% for now in 2024.

Lee Heng Guie is the executive director at Socio-Economic Research Centre (SERC) Malaysia.

- Focus Malaysia

The views expressed are solely of the author and do not necessarily reflect those of MMKtT.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.