The long-awaited award of digital banking licences has been made, but it raises some key questions with respect to who should own the licences, especially since there are conglomerates with other business interests who have been awarded the licence.

Over the years, the central bank, Bank Negara Malaysia, has made great strides in ensuring banking integrity by implementing strict control procedures as well as strict standards as to ownership of banks.

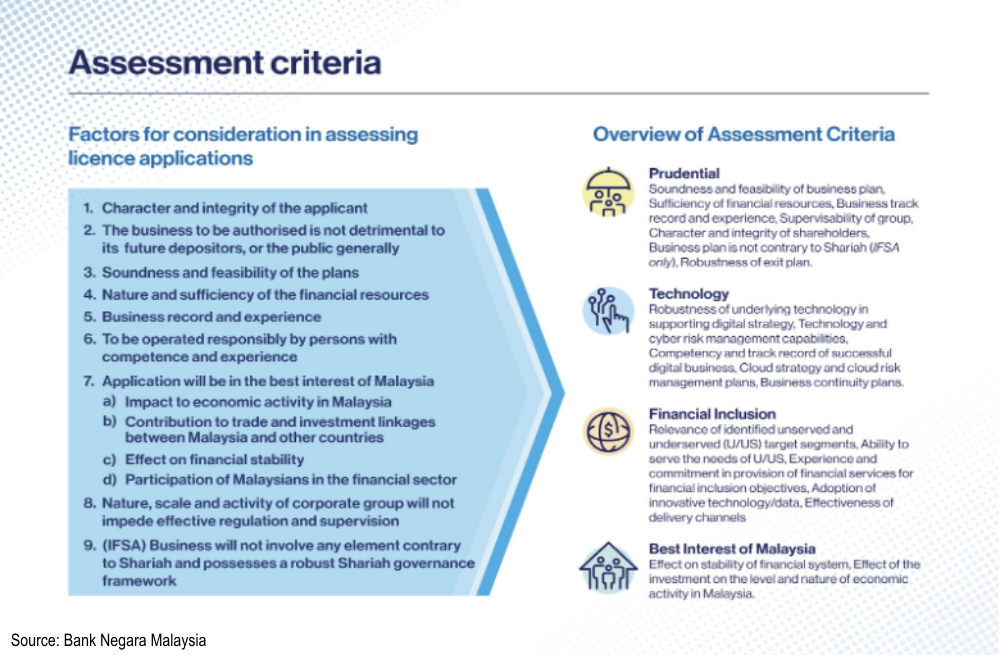

The assessment criteria for the selection of digital banks are given in the table below. For existing mainstream banks, the major shareholders cannot be involved in any other business but banking.

This started when Malayan Banking Bhd, the largest banking and financial group in the country, faced a major run on its deposits in the 1960s when it lent a substantial sum of its money to one of its major shareholders then, Khoo Teck Puat. The run was abated with Bank Negara's help.

Gradually, the ownership of all banks was restructured, and Bank Negara prevailed upon individual owners of banks to both reduce their holdings in the bank and to refrain from any other business so that there would not be conflict between their own business and that of the banks. The requirement gradually evolved over the years but is absent for digital banks.

Perhaps digital banks are seen as something new and different which will provide banking opportunities for those who currently are not bankable, mainly those who can’t get loans without security.

But it is hard to see how digital banks can close this gap considering that this is a rather tough business. The pawn-shop business, a key resort of the unbankable, requires security far in excess of the loans in the form of mainly gold jewellery.

I remember a Malaysian bank, United Asian Bank, since absorbed by the CIMB Group, used to offer jewellery loans, an indication that with some innovation, local banks could engage in this business.

The legal money lending business sets high-interest rates rivalling that of credit cards or even higher and has other back-to-back agreements to ensure recovery of money. In the worst cases, especially the illegal ones which charge extortionate rates, this includes coercion and threats. These have not deterred some desperate sections of the community from resorting to them.

Thus, the digital banking business, which basically seeks to make all banking digitalised, and online including approval and disbursement of loans, is not going to be a walk in the park and will pose great challenges to operations and profitability.

Even if there are substantial savings in staff costs by the digitalisation of the entire lending process and communications with customers, the control of bad debts is paramount, the risk of which has to be offset against potential returns. Human judgement cannot be replaced. Digital banking still remains largely untested and extreme caution is necessary.

Systemic risks

Of particular significance and concern is that the digital bank is also entitled to take deposits, although conditions require insuring these deposits as with mainstream banks where up to RM250,000 per account is insured. But unless these are carefully monitored, the potential for abuse is large.

The main concern is that if a cut-throat free-for-all competition emerges - both among digital banks and between digital banks and mainstream banks - then potentially, some of them could get into trouble posing systemic risks to the banking sector.

The one big change in the digital scenario is that Bank Negara has loosened the controls in ownership, allowing those who run other businesses to own these banks. While this may allow greater and quicker innovation, there are serious conflicts of interest with other existing businesses of the owners.

Five digital banking licences were granted by Bank Negara - picked out of a crowded field of 29. According to Bank Negara, the five as approved by the Minister of Finance are:

A consortium of Boost Holdings Sdn Bhd and RHB Bank Berhad.

A consortium led by GXS Bank Pte Ltd and Kuok Brothers Sdn Bhd.

A consortium led by Sea Limited and YTL Digital Capital Sdn Bhd.

A consortium of AEON Financial Service Co, Ltd, AEON Credit Service (M) Berhad and MoneyLion Inc.

A consortium led by KAF Investment Bank Sdn Bhd.

Three out of the five consortiums are majority-owned by Malaysians, namely Boost Holdings and RHB Bank Berhad, Sea Limited and YTL Digital Capital Sdn Bhd, and KAF Investment Bank Sdn Bhd.

Of the five, two are led by local financial institutions (RHB Bank, KAF), one by a foreign finance group (including AEON), and two by business conglomerates. It's the last two which raise the most concern.

Kuok Brothers is the well-known tycoon Robert Kuok-controlled holding company which has interests in a multitude of businesses such as property, logistics, maritime and hospitality, amongst others. They are solid, but they are a conglomerate and there can be conflicts.

The other is the one in which the YTL group is a partner. YTL is now a diversified group engaged in power, construction, hospitality, water, telecommunications and others.

It received a major boost when it became the first independent power producer in Malaysia via a 1993 power purchase agreement which gave it an extremely lucrative contract to produce power for electricity utility Tenaga Nasional Bhd. This happened over the strong and vehement objections of the utility’s then executive chairperson Ani Arope.

Digital banking seems to be all the buzz now, and while Malaysia needs to continue with changes taking place globally, it needs to watch itself. Some of these things can fizzle out - sometimes with a big bang which can cause a lot of damage.

Conservatism is an asset here, and it is worth remembering that only some will succeed in an industry which too many are entering.

Remember the dot.com boom and bust of the late 90s? Some have forgotten it already.

P GUNASEGARAM has written two books on banking and finance – ‘Bank Negara Malaysia: Bulwark of the Nation 1959-2017’ and a biography of the first Malaysian Bank Negara governor, ‘Tun Ismail Ali: Paragon of Trust and Integrity’. - Mkini

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.