The latest BN flagship roll out in election year is the attention grabbing Sara Rakyat 1Malaysia which is already very well explained in this post.

Kudos to the analyst for such an insightful piece of writing!

A responsible and proper government should be giving its people an environment where they can get good employment and business opportunity, clean and efficient governance. A responsible government should not be telling the deprived segment of population to borrow money and engage in equity investments.

The key selling point by BN administration is guaranteed return. No unit trust or investment manager in the world would dare to guarantee returns on investment.

Besides, if one is earning between RM500 to RM3,000, how much surplus that individual or family can afford to borrow and invest? They probably need a job and a fixed salary more, not some investments which pays a token RM50 a month but not immediately usable for buying household goods

Anyway, intrigued by the promise of “guaranteed return” I decided to find out more about this matter.

First stop, I looked up the Bernama news flash, which according to Tan Sri Hamad Kama Piah Che Othman, Group CEO of PNB, the scheme operates by way of investing into and getting paid in additional Amanah Saham 1Malaysia units.

This brings me to the next stop: the latest annual report and accounts issued by PNB on Amanah Saham 1Malaysia (AS1M).

There are approximately 271,000 Malaysians that invested RM5.5 billion into AS1Malaysia.

Now normally a complete set of financial statements should comprise a profit and loss account (or income statement),balance sheet and cashflow statement at a minimum.

Income statement would show you the income or loss for the year; the balance sheet would show how much asset and liability a company has while cashflow statement shows how the company’s money was used during the year. If you buy shares in Bursa Malaysia, you will get an annual accounts and reports from the listed company which runs into hundred of pages, even though you own 1,000 shares only.

But the report for this RM5.5billion trust money for Malaysians is very scarce. There is merely a Penyata Pendapatan dan Perbelanjaan and Penyata Pendapatan Komprehensif that is squeezed into 1 page plus a single page of Penyata Aliran Wang. The notes to the above ran from page 18 to 28 only. The scarcity of information could lead to difficulty in fully understanding what is actually going on with the funds.

The accounts tell you that AS1M made RM205.9 million and RM165.5 million over the 2 financial periods buying and selling shares, with only a minimal RM7.5 million diminution in value of shares purchased.

Normal accounting process requires shares purchased for buying and selling purpose to be “marked to market” e.g. if you buy 1,000 shares at RM5.00 in June and its price dropped to RM4.50 at 31 December when you close the accounts for reporting, then you have to report unrealised loss of (RM0.50 X 1,000) = RM500.

And with such volatile share price movements, how come for a RM5.5billion worth of trust money investment, the unrealized loss is barely 0.14% (RM7.5million over RM5.5 billion).

In addition, notice how small the operating expenses is to run a RM5.5 billion trust fund. Not counting the yuran pengurusan which goes to the fund managers, administration support only runs up to RM447,186 and RM420,540; about RM30K to RM37K a month.

The audit fee of RM20,000 is absurdly low. Low fees mean low quality audit – ask any auditors and they will tell you the same thing. RM20,000 audit fee is likely for a medium size company, not for a RM5.5 billion trust fund of rakyat’s money being invested in risky and volatile equity market.

It is amazing to see how AS1M make such great profits. Normal unit trust companies would not be able to match them. My personal experience with unit trusts tells me that making losses over a few years is normal.

There is no balance sheet hence we cannot tell what is the asset and liability of the funds. Now for the fund to make consistent above market gains, I would very much like to know to whom they sold the shares (i.e. their trade debtor assets).

It seems that for the first year in operation, they sold more than half of the shares back to PNB. Is this a right pocket to left pocket thing only?

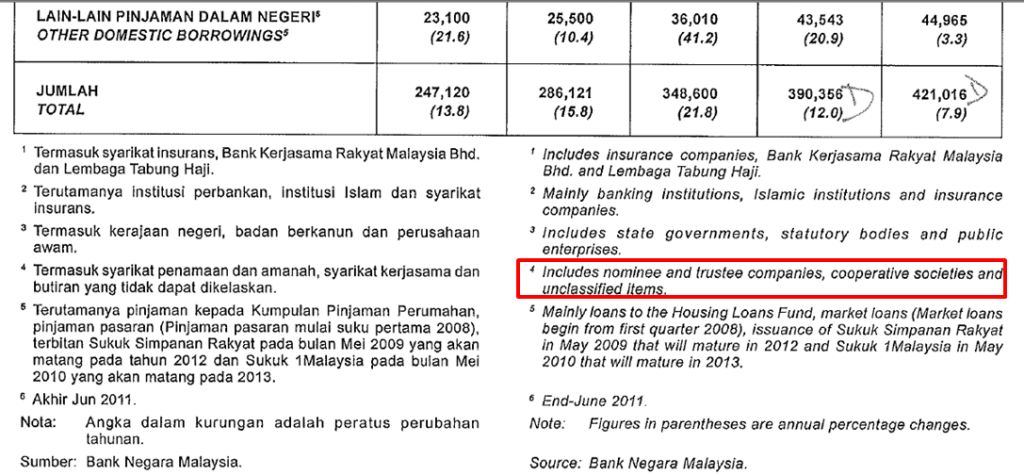

In my previous blog post on national debts, I am intrigued by the rapid raise of a component in Hutang Dalam Negeri Persekutan called “Lain-lain”. This nugget shot up from RM39,781 million to RM111,856 million in 2011! Increase of around 2.8 times over 4 years. It has taken over from EPF as the biggest amount owing to.

Now according to Bank Negara's definition, it includes “trust companies” and “unclassified items”

AS1M is a trustee as it invests billions of rakyat moneys around. The AS1M report does not have a balance sheet so Icannot confirm whether that part of national debt has anything to do with a debt arising as a result of buying shares from AS1M but I definitely DO NOT WANT TO BE A GUARANTOR FOR SHARE MARKET SHORTFALL. Guaranteeing the profit of toll concessionaires is already taxing enough.

Perhaps the finance minister should come out and clarify who we are owing to and what for.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.