Najib Abdul Razak and his son Mohd Nazifuddin succeeded in obtaining an apex court order to stay the tax-related summary judgment against them.

A three-person Federal Court bench chaired by Chief Justice Tengku Maimun Tuan Mat unanimously allowed the stay application, following no objection raised by the Inland Revenue Board’s (IRB) legal representative, senior federal counsel al-Hummidallah Idrus.

The panel - also comprised of apex court judges Mary Lim Thiam Suan and Rhodzariah Bujang - granted the stay pending disposal of the hearing of the merits of the appeal by the former prime minister and Nazifuddin before the Federal Court.

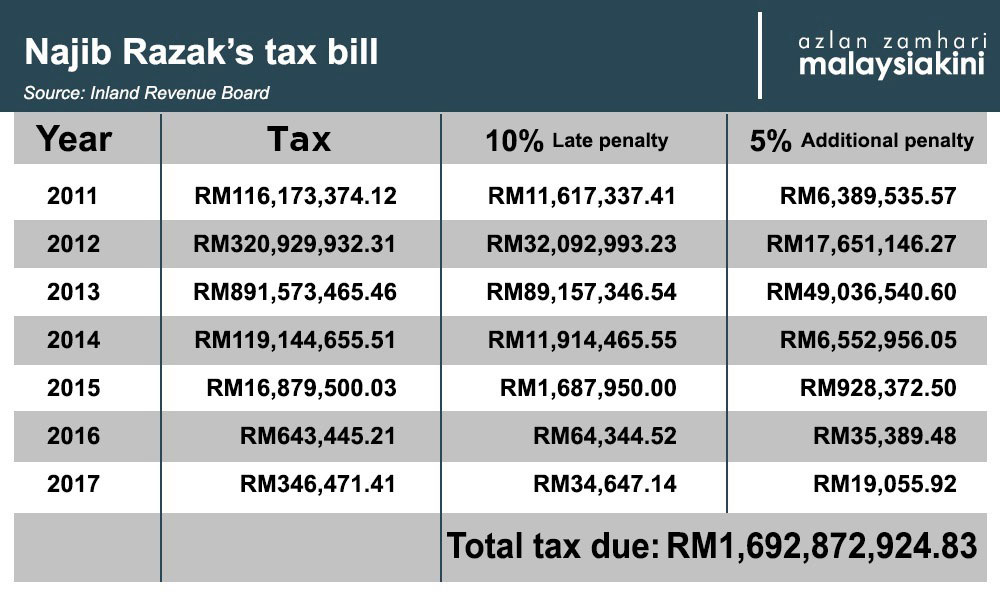

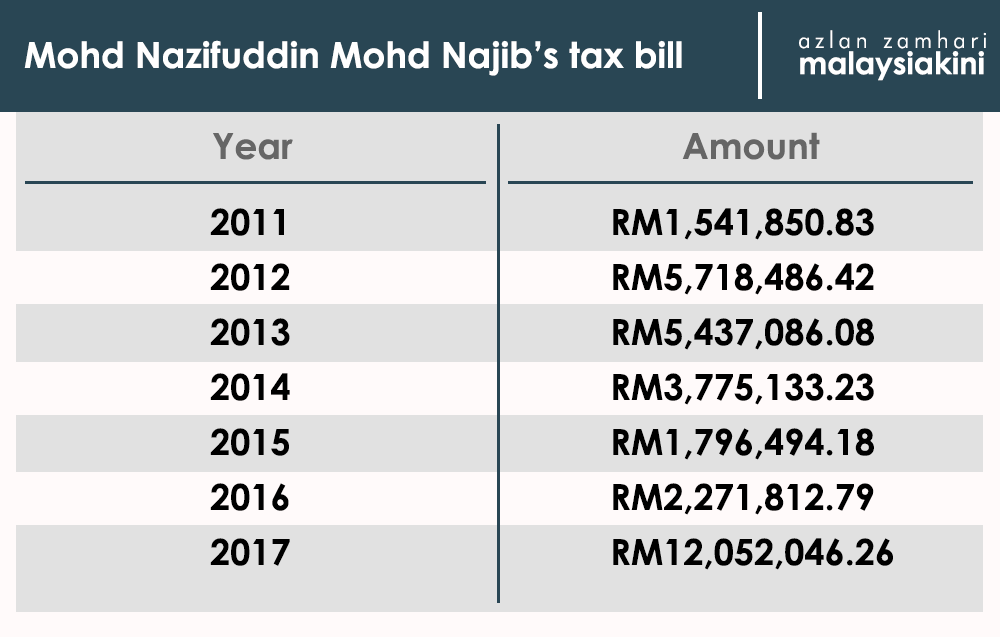

The summary judgment, issued by the Kuala Lumpur High Court in 2020, allowed the IRB’s civil action to seek RM1.69 billion and RM37.6 million from Najib and his son respectively while dispensing with the need to consider the duo’s defence against the suit.

The duo’s appeal before the apex court basically seeks for them to quash the summary judgment and be allowed to present their defence against the tax suits.

Najib and Nazifuddin failed in an earlier appeal before the Court of Appeal on Sept 9 last year to reverse the summary judgment.

Back on May 10 this year, the father and son obtained leave from the apex court to proceed with their appeal.

The Federal Court, however, has yet to set a date to hear the merits of the main appeal, with the matter fixed for further case management tomorrow.

The bankruptcy proceedings, commenced by IRB against Najib and Nazifuddin before the Kuala Lumpur High Court, are also currently stayed, pending disposal of the duo’s main appeal.

No objection

During online proceedings earlier this morning, the duo’s counsel Muhammad Farhan Muhammad Shafee informed the apex bench that the respondent (government through the IRB) has no objection to the stay application.

When Tengku Maimun asked the tax authority’s representative, al-Hummidallah confirmed that they are only agreeable to the stay being in place until the disposal of the main appeal by Najib and his son.

The panel then allowed the application, ordering for costs to be the cost in the cause.

Under civil litigation, the cost in the cause means the unsuccessful party has to pay the costs of the party that succeeded later in the main legal matter.

One central issue in the appeal is whether Section 106(3) of the Income Tax Act 1967 (ITA) is invalid for contravening Article 121 of the Federal Constitution.

Section 106, in general, empowers the IRB to institute a civil action in court to recover tax arrears and penalties from taxpayers.

Section 106(3) specifically states that in relation to IRB’s civil action to recover taxes, the court “shall not entertain any plea that the amount of tax sought to be recovered is excessive, incorrectly assessed, under appeal or incorrectly increased”.

Article 121 is in relation to the powers of the judiciary in Malaysia.

In their appeals, Najib and Nazifuddin’s legal team contended that Section 106(3) is unconstitutional as it takes away the court’s power (as per Article 121) to consider the defence of a taxpayer against the IRB’s civil actions to recover the tax. - Mkini

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.