MAHB deal: Merging control through public-private partnerships

Two events over the past month have raised more troubling questions about the proposed privatisation of Malaysia Airports Holdings Bhd (MAHB), a publicly listed GLC.

One event occurred abroad, at the G7 meeting in Italy, while the other was when Prime Minister Anwar Ibrahim responded to queries about the MAHB controversy.

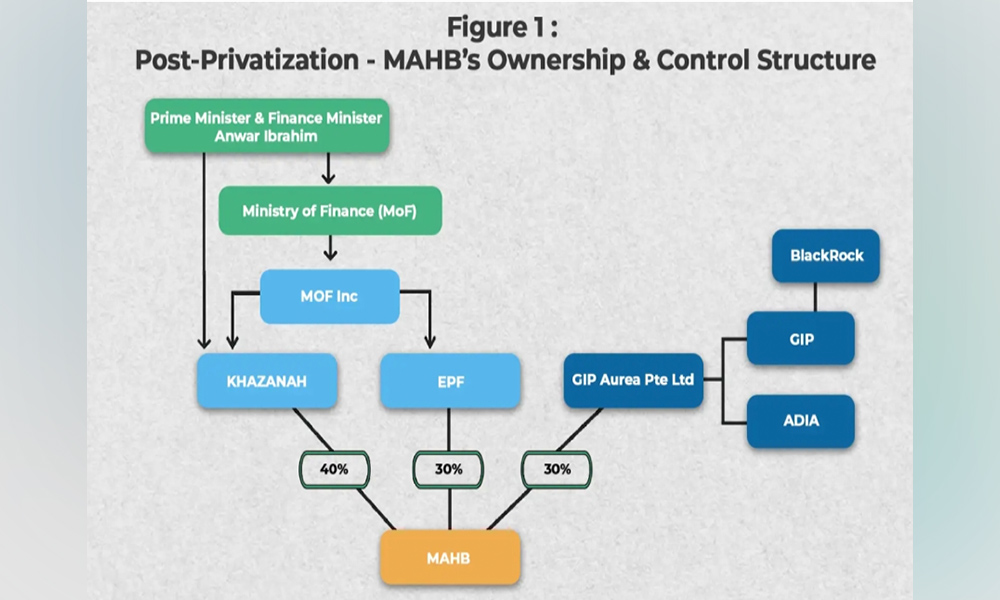

MAHB’s major shareholders are three government-linked investment companies (GLICs) - Khazanah Nasional (33 percent stake), Employees Provident Fund (7.9 percent) and Kumpulan Wang Persaraan (Kwap) (4.9 percent).

If MAHB is privatised, Khazanah will emerge as its largest shareholder with a 40 percent stake, with EPF owning 30 percent.

The controversy surrounding MAHB’s privatisation is that the remaining 30 percent equity will be owned by GIP Aurea Pte Ltd, a joint venture between Global Infrastructure Partners (GIP) and Abu Dhabi Investment Authority (ADIA) (see Figure 1).

GIP will own 88.33 percent of GIP Aurea’s equity, effectively giving it a substantial minority 25 percent interest in MAHB.

In January this year, BlackRock, the world’s largest asset fund manager, announced its intention to acquire GIP, a deal valued at US$12.5 billion.

GIP, a major infrastructure investor, owns companies worldwide in a variety of sectors including energy, infrastructure and airport management. After its takeover of GIP, BlackRock will also emerge as the world’s second-largest infrastructure investor, enhancing its presence as a global multi-sector asset manager.

Controversial statements

At the G7 meeting, Larry Fink, the CEO of BlackRock, stressed four points:

Capital markets, not multi-lateral banks, are the largest source of private-sector financing while building new infrastructure is vital.

Thus, the need to unlock more private capital for infrastructure in emerging nations.

Public-private partnerships are essential to allow for private funding of infrastructure.

BlackRock’s infrastructure focus is airports and data centres for artificial intelligence.

In keeping with Fink’s focus on infrastructure, BlackRock moved to acquire GIP.

The second event occurred when Anwar addressed the MAHB controversy in Parliament. He made the following points:

The cabinet does not interfere in investment decisions by Khazanah and EPF. And, these GLICs “do not refer to the executive arm of government before making decisions”. He will inform his cabinet of MAHB’s privatisation after the negotiations are completed.

Foreign companies now own 27 percent of MAHB’s equity. These shares will be taken over by GIP Aurea.

MAHB’s privatisation will not compromise national security because this “exercise only involves management. MAHB is the company that manages the airports, (and) the airports remain the property of the Malaysian government.” MAHB’s top management positions, the chairperson and chief executive officer (CEO), will still be held by Malaysians.

While Fink’s call for public-private partnerships for infrastructure financing should be treated with caution, Anwar’s statements draw attention to a distinct lack of transparency and accountability in the governance of GLICs and GLCs.

Decision-making control: GLICs and GLCs

When Anwar disclosed that the cabinet did not discuss MAHB’s privatisation, he inadvertently revealed the extensive concentration of decision-making control in his hands.

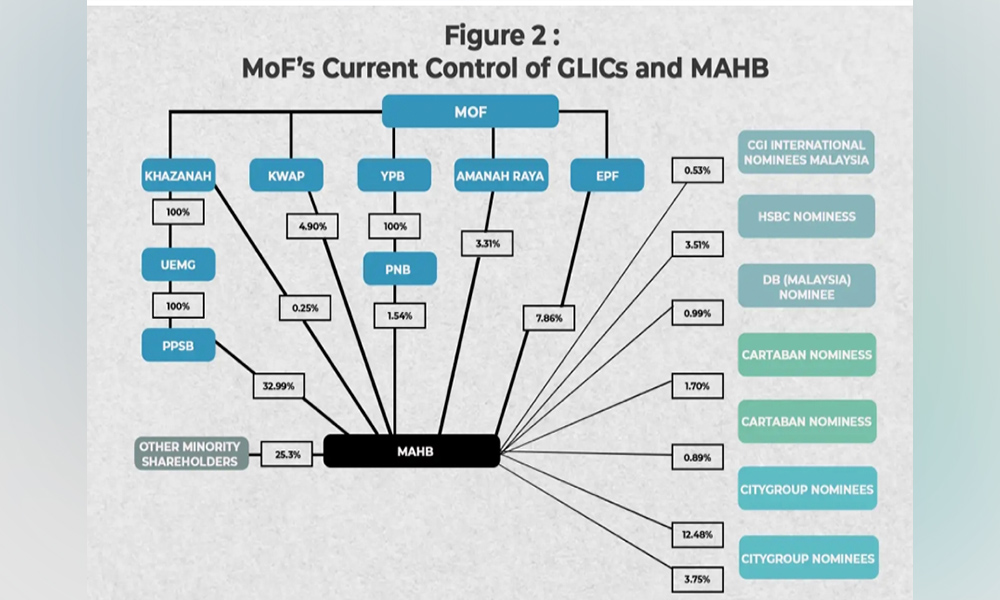

As Figure 1 reveals, control of Khazanah and EPF is, ultimately, in the office of the finance minister, through the government’s equity holding company, Minister of Finance Incorporated (MoF Inc.).

As prime minister, Anwar also chairs Khazanah’s board of directors. Since Anwar concurrently serves as prime minister and finance minister, this deeply undermines checks and balances in the executive arm of government.

Prime Minister Anwar Ibrahim

Given the finance minister’s control of the GLICs and important GLCs such as MAHB, three public governance questions arise.

Did the Khazanah’s board of directors and EPF have the autonomy to decide on MAHB’s privatisation? Did both boards independently concur that GIP Aurea should secure a substantial minority 30 percent stake in this GLC that manages 39 international and domestic airports in Malaysia? Are these directors aware that if GIP Aurea obtains a 30 percent stake in MAHB, BlackRock will secure indirect control of this GLC?

Anwar stressed BlackRock’s huge ownership of Malaysian corporate equity, totalling RM20.5 billion. BlackRock has an equity interest in about 100 listed firms, including in GLCs such as Tenaga Nasional and Telekom Malaysia.

However, BlackRock does not have a substantial minority interest in any of these enterprises. Moreover, the 27 percent MAHB equity now under foreign ownership is widely dispersed, with no institution having a substantial minority interest in this GLC (see Figure 2).

MAHB’s privatisation entails a public-private partnership (PPP), the type of tie-up that Fink appears to be actively advocating.

This PPP may well result in an indirect link between two powerful figures. The first is a prime minister governing a huge GLC ecosystem where considerable economic power is concentrated, with decision-making control centred in his hands.

As for Fink’s financially well-endowed BlackRock, its indirect entry into MAHB will give it a major presence in Malaysia’s airports. Does this PPP portent BlackRock’s direct or indirect entry into other sectors, including energy and data centres?

Management control by GIP?

GIP’s portfolio of activities includes managing airports, the stated reason for its presence in MAHB’s privatisation. GIP is, in fact, the only enterprise in MAHB’s restructured ownership consortium that has any experience managing airports.

This means that even if MAHB’s chairperson and CEO are Malaysians, its day-to-day management will inevitably be in GIP’s hands. Why is Khazanah offering a foreign firm management control of Malaysia’s airports?

There are other troubling questions.

Would government regulators - Immigration and Customs and the Civil Aviation Authority of Malaysia (CAAM), be willing to work with - and provide information to - a foreign enterprise when dealing with security matters?

GIP will have to work closely with another GLC, Malaysia Airlines (MAS), also under Khazanah’s control. Was MAS consulted in MAHB’s privatisation exercise?

The poor management of MAHB has been a longstanding problem. Why has Khazanah not rectified this problem by bringing in international consultants with relevant expertise, instead of offering GIP huge equity ownership and management control of MAHB?

Fink is quite open about BlackRock’s desire to use PPPs to secure access to core sectors in emerging economies, including airports. Should not Anwar be wary of a BlackRock-linked PPP that involves MAHB?

Reform GLC ecosystem

This MAHB-Khazanah-EPF controversy serves as another instructive reason why Malaysia’s vast GLC ecosystem, historically a persistent site of extreme abuse of power and corruption, requires urgent reforms.

This controversy also suggests why Anwar has been reluctant to institute these reforms. As Anwar himself has disclosed, in the executive arm of government, he can solely decide on major GLC exercises, including questionable PPPs, a method of executive decision-making control that must be rectified.

Importantly too, as prime minister-cum-finance minister, Anwar has enormous influence over the boards of directors of GLCs, giving him indirect management control.

Thus, Anwar can solely decide who to appoint as GLC directors, including sitting parliamentarians, a practice he strongly criticised when he was opposition leader. - Mkini

EDMUND TERENCE GOMEZ is former professor of political economy at Universiti Malaya.

The views expressed here are those of the author/contributor and do not necessarily represent the views of MMKtT.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.