THE RIPPLE effects of a US-Iran conflict extend well beyond the battlefield, quietly driving up costs and exposing dependencies in global supply chains.

For Malaysia, the impact sits at a delicate crossroads between relatively stable logistics and vulnerabilities higher up the production chain.

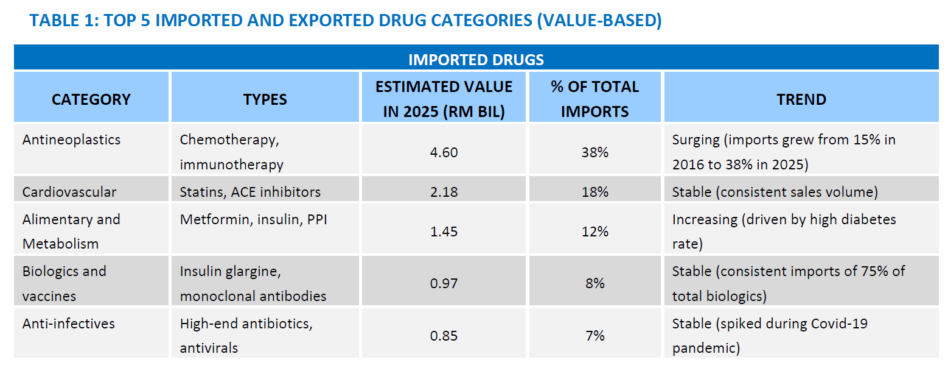

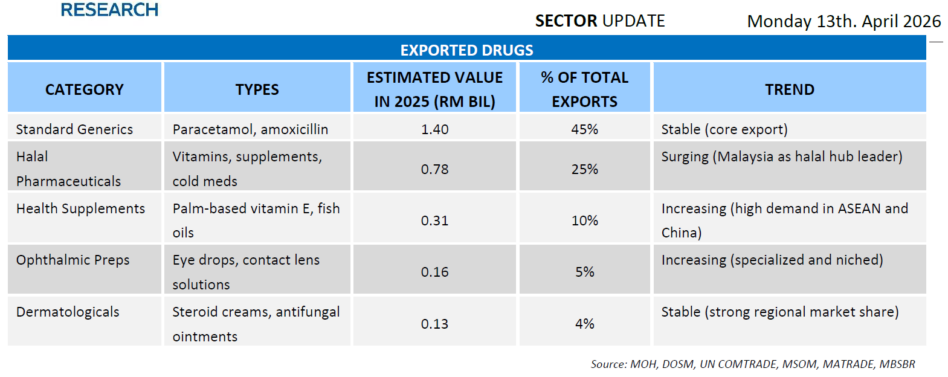

Much of the country’s supply resilience is shaped by geography. The Malaysian Association for Pharmaceutical Suppliers (MAPS) notes that about 30% of Malaysia’s pharmaceutical suppliers are based in India, with others located in countries such as South Korea and Germany.

While shipments to Malaysia largely bypass the Strait of Hormuz, the picture is more complex upstream.

India, Malaysia’s main source of generic medicines, depends heavily on the Strait for petroleum-derived inputs and energy needed to power its manufacturing sector.

Any disruption that drives up production costs there could quickly filter through the supply chain.

In such a scenario, Malaysia’s estimated RM1 bil in savings from switching to generics may be wiped out, especially if prices surge by as much as 50%.

Beyond the pills, the crisis also affects the invisible components of the pharmaceutical industry.

This includes aluminium and plastics. About 9% of global aluminium comes from the Middle East.

Shortages of these two elements could affect the production of blister packs that housed most generic drugs.

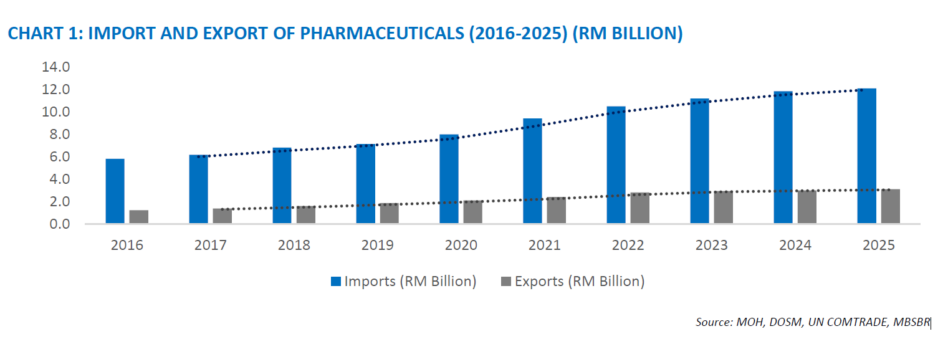

Based on 2025 trade numbers, Malaysia had reached a historic trade milestone although the deficit is still significant.

Pharmaceutical imports were valued at roughly RM12.1 bil, an increase of +2% year-on-year (yoy), while exports totaled at about RM3.1 bil(+4%yoy).

However, this still shows that Malaysia remains a net importer of drugs, notably since 2020 (during the Covid-19 pandemic) when the import bill nearly doubled.

Major MOH drug suppliers had since voiced concerns, indicating that a 50% increase in raw material costs could make MOH’s fixed-price contracts economically unviable for suppliers, potentially leading to the use of force majeure to exit or renegotiate agreements.

The most worrying development for the public sector is the advice from suppliers for hospitals to order early. This potentially could create a pre-emptive shortage scenario.

If district hospitals, especially in East Malaysia, begin stockpiling to avoid the price hike, it would deplete the national 5-month buffer stock faster than initially expected.

Meanwhile, suppliers are now moving towards an allocation model that allows them to be selective on which hospitals would get the drugs based on availability rather than relying on patient volume. This would risk critical shortages in rural areas.

The immediate impact on a company level may be evident in Pharmaniaga Bhd (BUY, TP: RM0.36), though we noted that it is a rather paradox situation of high strategic importance versus intense financial pressure. Pharmaniaga is seen to be the national shock absorber.

Under the 10-year concession renewal (up to 2033), the group is contractually obligated to maintain at least 2 months of additional buffer stock beyond the hospitals’ inventories.

While Pharmaniaga holds adequate stock for now, the industry is currently debating who is the bearer of the cost for the higher buffers, as storing 3-6 months’ worth of medicine requires consistent climate-controlled warehouses, as well as additional capital, which could strain the group’s finances.

The advantage to this, however, is that the group has a crucial role to fulfill, as the MOH would highly rely on Pharmaniaga’s logistics network to manage the prudent distribution and rationing as suggested, consequently cementing the group’s 10-year security in the market. — Focus Malaysia

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.