MP SPEAKS | Malaysia’s digital transformation ambitions, while admirable, have hit the proverbial wall even before they could take off.

To begin with, energy-guzzling data centres make little sense when we are a net crude oil importer and when coal-fired power plants remain our main source of electricity.

At the same time, the water needed for cooling these data centres directly competes with domestic and agricultural use, undermining our quest for food security.

Never mind our artificial intelligence (AI) aspirations, where we have once again shot ourselves in the foot by allowing the historic 10‑year strategic partnership with UK-based Arm Holdings PLC, which was meant to bolster local AI chip design and front-end semiconductor capabilities, to be undermined by allegations of impropriety.

Unless the government sheds its lackadaisical attitude towards corruption and mismanagement allegations, which are damaging our international reputation, our dream of moving up the chip-making value chain might well go down the drain.

We must not allow the 2024 National Semiconductor Strategy to be diminished to the point that it is not even worth the paper it is printed on.

Macroeconomic necessity

The formal inclusion of nuclear energy in the National Energy Transition Roadmap (NETR) and the 13th Malaysia Plan (2026–2030) is not merely a policy shift; it is a macroeconomic necessity made even more urgent by the ongoing conflict in West Asia.

While the dissolution of the Malaysia Nuclear Power Corporation (MNPC) in 2019 was a major setback, we are once again seeing a healthy appetite for rebuilding our capacity to introduce nuclear energy into our energy mix.

Despite our obsession with green energy sources under the NETR, experts across the energy sector broadly agree that only nuclear power can provide the secure baseload needed to make renewable energy (RE) truly viable in the long run.

Taking a leaf out of the US–China trade dispute, it might be best to address the elephant in the room in earnest.

China’s ban on rare earth elements (REE) exports is a direct hit on US chip ambitions and, perhaps less obviously, is also hurting its military-industrial complex, which relies heavily on advanced chips.

Malaysia faces a limited uranium supply, and our identified deposits are far too small to sustain a commercially viable nuclear power programme. We are also spatially challenged, as aggressive urban sprawl makes land an even more precious commodity.

However, recent developments have made two options scientifically viable. The first is the small modular reactor (SMR), which could potentially supplant our environmentally polluting coal power plants in carefully orchestrated stages.

The second is to harness the abundance of thorium, often a by-product of REE mining, which can be treated to produce fissile uranium.

In this respect, the conventional gigawatt-scale uranium reactor becomes a much less attractive option. The future of firm, zero-carbon baseload power most likely lies in SMRs, specifically those fuelled by locally mined thorium.

Escaping the energy importer trap

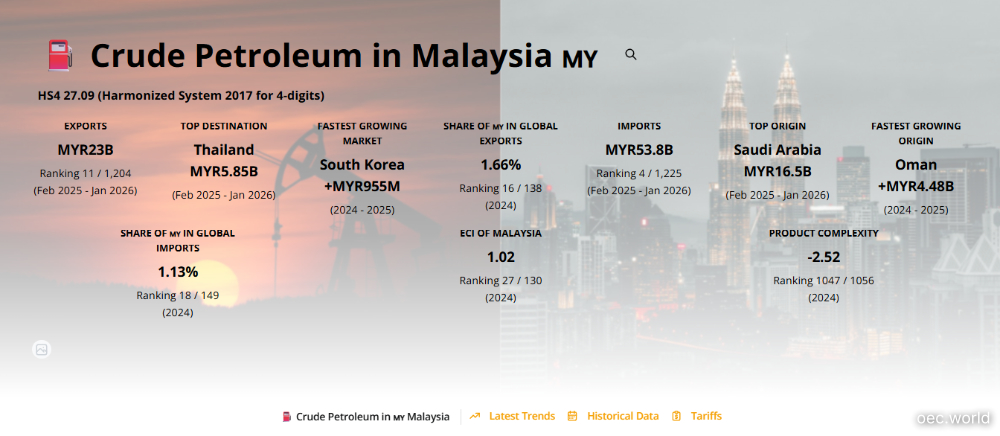

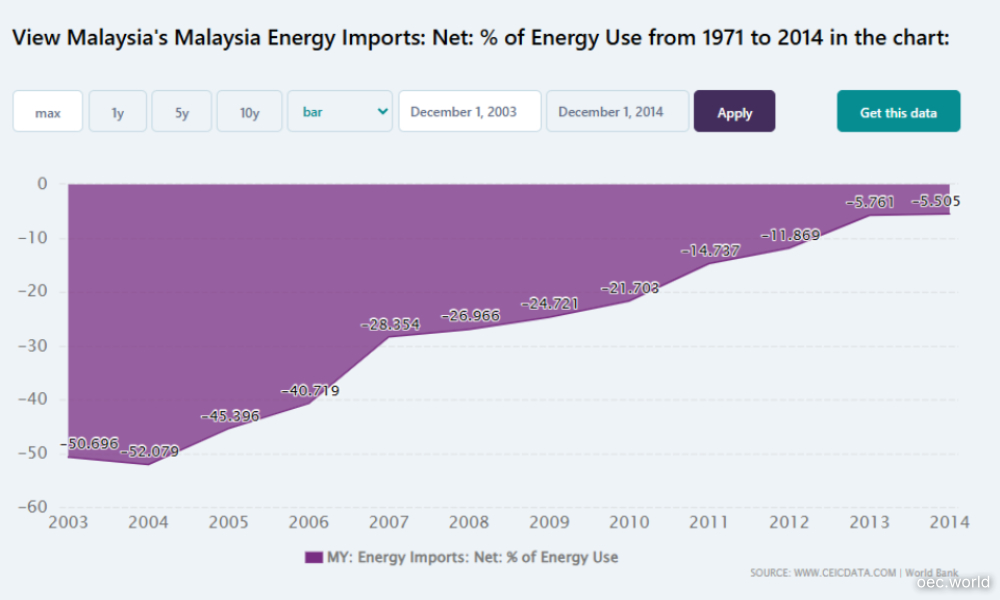

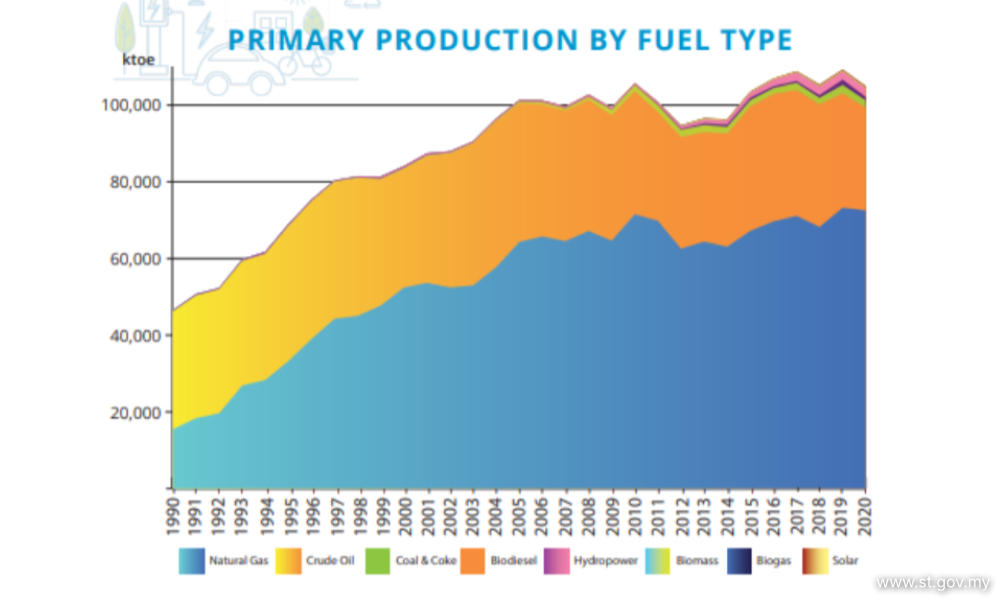

Malaysia’s historical reliance on domestic oil and gas is fast approaching its expiry date. With maturing fields and dwindling production, data trajectories point to a structural vulnerability: Malaysia, already a net crude oil importer, is slowly but surely transitioning toward becoming a net energy importer as well.

As domestic consumption surges, relying on imported coal and gas exposes Putrajaya to immense foreign exchange volatility and supply chain shocks.

At the current trajectory, even our supposedly secure coal imports, which supply a large share of our electricity, may become unreliable as source countries put their own national interests above export-driven commercial returns.

The NETR has, perhaps ambitiously, targeted a 70 percent RE capacity mix by 2050. However, let us be candid about the physics and economics of this: solar and wind are intermittent, and especially so in Malaysia, where our current energy storage technology is grossly insufficient.

The RM1.85 trillion investment needed to achieve this must come from somewhere and, in today’s climate, it is highly unlikely that oil wealth will be able to contribute significantly.

Even if it does, trading reliance on fossil fuels for dependence on lithium and cobalt supply chains carries its own severe environmental and geopolitical toxicities.

Without firm, zero-carbon baseload power, such ambitions would leave the nation increasingly beholden to foreign powers for its energy survival.

Turning liability into sovereignty

Remarkably, Malaysia already possesses a latent strategic advantage: an indigenously abundant supply of thorium. Decades of REE processing - from the historical operations of Asian Rare Earth in Bukit Merah, Perak, to modern facilities in Pahang - have generated substantial stockpiles of thorium by-product.

Historically viewed as an environmental liability and a source of public anxiety, this thorium surplus can be refined into a sovereign fuel bank. This flips a long-standing grievance into the foundation for future energy independence.

To understand the business case, one must first strip away the emotive baggage of the 20th-century nuclear industry.

Chernobyl was a case of local politics disregarding science and overriding the public interest, while the Fukushima incident was shaped by cultural and institutional entanglements that modern technology could otherwise have mitigated.

Unlike conventional pressurised water reactors, molten salt reactors (MSRs) using thorium-based fuels operate at near-atmospheric pressure.

In the event of a power failure, there is no high-pressure coolant to boil off; the liquid fuel simply drains into a passive cooling tank and solidifies, making a Fukushima-style meltdown far less likely.

The thorium fuel cycle produces a fraction of the long-lived radioactive waste associated with uranium. Furthermore, its by-products are inherently not weaponisation-friendly, sidestepping global proliferation anxieties.

SMRs are designed to be factory-built, transported to site, and scaled incrementally. This modularity sharply reduces the decade-long delays, cost overruns, and capital risks that have historically plagued nuclear megaprojects.

Furthermore, nuclear energy is the most land-efficient power source: it requires 18 to 34 times less land per unit of electricity than ground-mounted solar PV.

For land-constrained regions like Malaysia, sacrificing our millennia-old rainforests for solar farms would be a profound environmental paradox.

Strategic partnerships that pay

China is the undisputed global leader in thorium MSRs, having successfully operationalised its TMSR‑LF1 prototype in 2025 and now rapidly scaling toward commercial deployment.

It aggressively expanded its nuclear and renewable capacity because it had anticipated a now‑proven fatal vulnerability: over‑reliance on the Strait of Hormuz for energy imports.

Recent developments make a strong case for Malaysia to adopt the same survival mindset - but at a far more strategic level.

India possesses the world’s most advanced thorium fuel‑cycle expertise, driven by its decades‑long, three‑stage nuclear programme and vast domestic reserves.

Russia, meanwhile, holds an unparalleled track record in the commercial deployment of SMRs, including advanced floating variants.

Japan’s recent nuclear revival and its deep expertise in advanced reactor engineering make Tokyo an indispensable partner. Collaborating with Japan also opens access to low‑cost, long‑term financing from institutions such as the Japan Bank for International Cooperation (JBIC).

Japan leads the Asia Zero Emission Community (AZEC), an initiative uniting 11 nations - including Australia and Asean members - to accelerate continental decarbonisation.

Malaysia should seize this momentum, capitalising on the grants, investments, and technical expertise Japan brings to the table.

In particular, we should engage Tokyo to leverage its advanced nuclear technologies and power‑generation capabilities.

Overcoming regional paralysis

Asean’s overall macroeconomic growth hinges on achieving genuine energy sufficiency. Energy-starved neighbours like Singapore and rapidly industrialising regions in Indonesia represent massive, captive export markets for clean, carbon-free power.

While an Asean-level energy consortium is theoretically ideal, mega-infrastructure projects often stall for decades under policy decisions that require slow, consensus-based approvals - the Asean way.

Despite these constraints, Malaysia’s position is uniquely advantageous. As a politically stable, rapidly industrialising economy with a desperate need for clean baseload power, a robust regulatory sandbox, and direct access to the broader Asean market, Malaysia’s infrastructure is an ideal launchpad for a regional consortium that pioneers the export of clean, modular power to the Global South. - Mkini

WAN AHMAD FAYHSAL WAN AHMAD KAMAL is the MP for Machang and a member of the Parliamentary Special Select Committee on International Relations and International Trade.

The views expressed here are those of the author/contributor and do not necessarily represent the views of MMKtT.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.