Taxpayers urged to seek clarity from LHDN

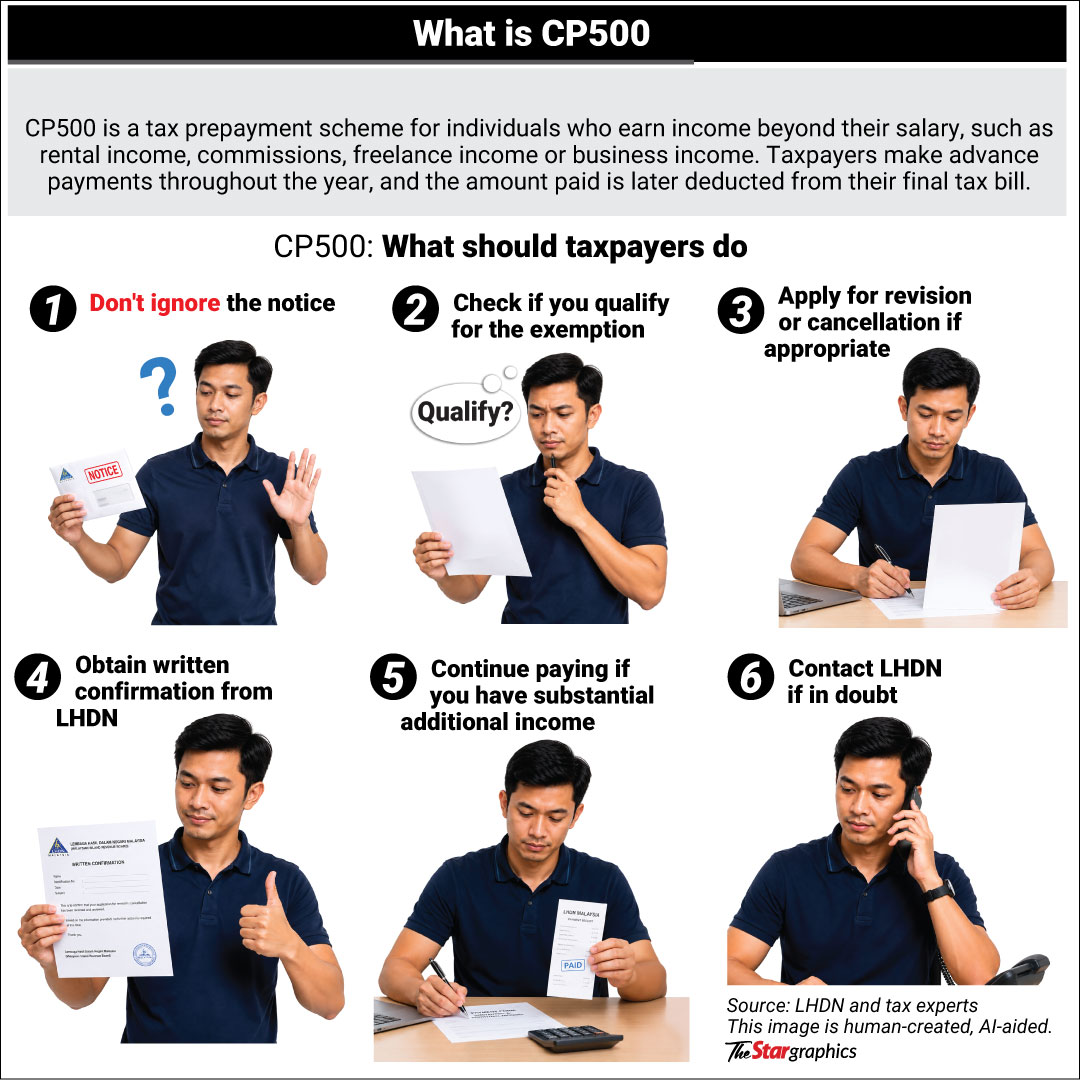

PETALING JAYA: Taxpayers should not ignore CP500 notices or assume they are automatically exempt from penalties, say tax experts, amid confusion over who qualifies for the government’s relief measure and when penalties may still apply.

They advised taxpayers to seek clarification from the Inland Revenue Board (LHDN), apply for cancellation where appropriate or obtain written confirmation of any exemption rather than rely on their own interpretation of the rules.

The issue arose after a recent clarification by LHDN that some taxpayers may still face a 10% penalty under the Income Tax Act, despite the government’s CP500 penalty relief announced in January.

It said taxpayers who do not fully pay their instalments, pay late or pay less than the required amount may still be subject to the penalty, raising questions over the scope of the exemption.

Tax consultant Datin Christine Koh said LHDN’s clarification on CP500 penalties was not surprising but could be confusing for the general public.

She noted that some taxpayers had understood the penalty exemption as applying broadly to all recipients of CP500 notices.

“Some of our sole proprietorship and partnership clients had already asked back in January whether they were also exempted from CP500 penalties,” she said in an interview yesterday.

The managing director of Owen KLCA Plt said the relief appeared to be aimed mainly at taxpayers receiving CP500 notices for the first time, particularly those with employment income and additional income sources such as rental income, commissions, freelance work or side businesses.

Historically, employment income is already subject to the monthly tax deduction (PCB), and some taxpayers with additional income may not have received CP500 notices previously.

However, LHDN is now expanding the use of CP500 to collect advance tax on income that is not covered by PCB, she said.

As a result, many taxpayers with salary income and side income may be receiving CP500 notices for the first time.

“Taxpayers should first determine whether they qualify for the exemption.

“For first-time recipients who believe the estimated tax amount is excessive, they may apply to revise the CP500 amount downward or even to zero where appropriate,” she said.

However, Koh cautioned taxpayers against assuming they can simply disregard the notices.

“If the taxpayer genuinely has substantial additional income and the CP500 amount is reasonable, it is advisable to continue paying according to the instalment schedule instead of relying on the penalty waiver,” she said.

Tax expert Datuk Koong Lin Loong agreed that the relief announced earlier this year appeared to be intended mainly for taxpayers receiving CP500 notices for the first time, particularly those with employment income and side income.

However, he warned taxpayers to exercise due diligence rather than just assume they were covered by the exemption.

“If they believe the notice was issued in error, they should approach LHDN and apply for cancellation instead of simply ignoring it,” he said, adding that taxpayers with additional income who receive CP500 notices generally have a responsibility to pay the instalments.

Koong also called for greater clarity from LHDN on the scope of the exemption.

“LHDN needs to further clarify the exemption so taxpayers can better understand how to deal with CP500,” he said. - Star

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.