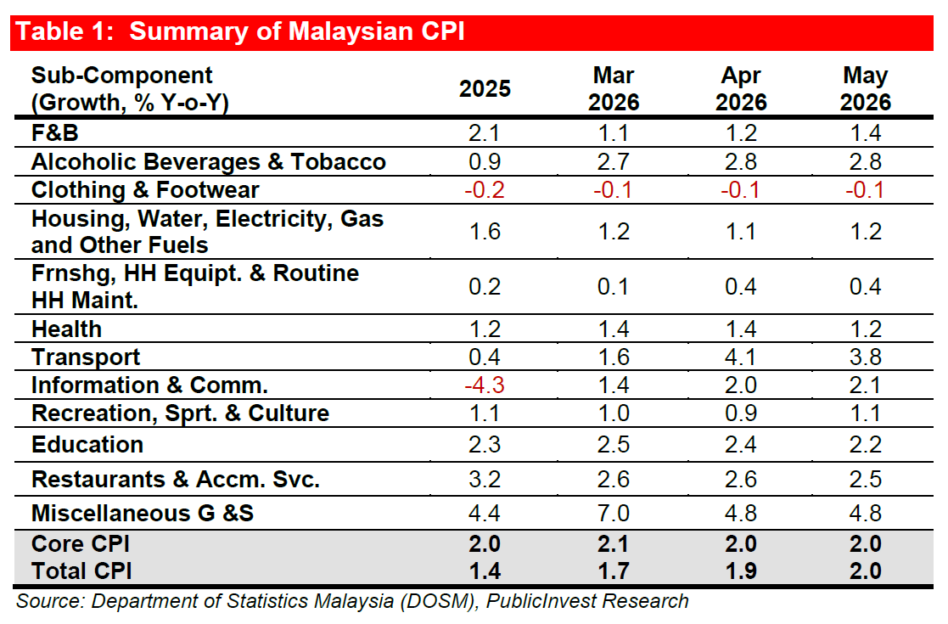

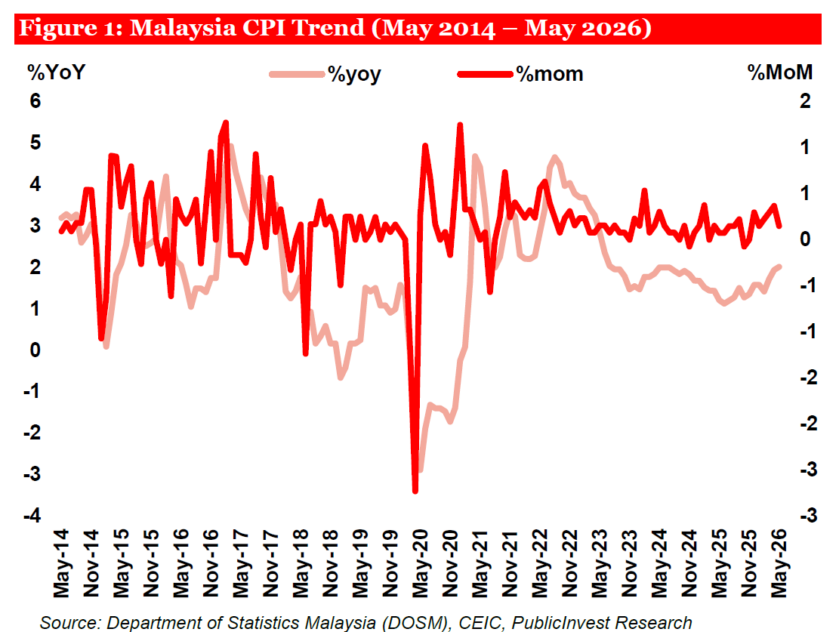

MALAYSIA’S headline CPI edged up to +2.0% year-on-year (YoY) in May from +1.9% in April, while core CPI was unchanged at +2.0% YoY and inflation excluding fuels rose to +1.8% from +1.7%.

“We maintain our 2026 CPI forecast at +2.4% YoY and keep our OPR call at 2.75% through 2026, although the balance of risks has become less comfortable,” said Public Investment Bank (PIB).

PIB maintains that inflationary pressures remain largely cost-driven rather than fuelled by stronger consumer demand, although rising costs are now extending beyond oil prices to broader supply-chain and production expenses.

While underlying inflation remains manageable at present, uncertainty surrounding the US-Iran Memorandum of Understanding (MoU) continues to cloud the external cost environment, leaving the outlook vulnerable to fresh shocks.

Domestic fuel subsidies are expected to mitigate the immediate impact on households.

However, the potential spillover of higher costs into food prices, utilities and transportation poses a significant risk in the second half of 2026.

As a result, Bank Negara Malaysia (BNM) is likely to maintain its current policy stance unless inflationary pressures become more widespread and entrenched across the economy.

Malaysia’s headline CPI edged up to +2.0% YoY in May 2026 from +1.9% in April, driven by firmer increases in Information & Communication, Food & Beverages, Housing-related components, and Recreation, Sport & Culture.

This was partly offset by softer Transport and selected services inflation, while Clothing & Footwear remained in mild deflation at -0.1%.

“We think the May outcome still reflects a selective firming in prices rather than a broader build-up in underlying inflation pressure,” said PIB.

State-level inflation remained broadly benign in May, with most states still below the national headline rate of +2.0% YoY. Sarawak recorded the lowest pace at +0.5% YoY.

Still, eight states printed above the national average, led by Pahang at +2.8%, followed by Negeri Sembilan and Wilayah Persekutuan Labuan at +2.6%, Johor at +2.5%, Wilayah Persekutuan Kuala Lumpur at +2.4%, and Kedah, Wilayah Persekutuan Putrajaya, and Melaka at +2.2% to +2.1%.

The recent US-Iran MoU briefly eased near-term oil pressure, but its implementation remains fragile and the latest tensions around Lebanon and the Strait of Hormuz suggest the external backdrop is still unstable rather than clearly improving.

Fuel subsidies should continue to soften the direct household impact, but they do not fully insulate the broader basket if higher costs in the supply-chain inputs begin to feed through more visibly in 2H26.

For now, that should leave BNM on hold unless price pressures start to spread more clearly beyond the current cost-driven pockets. — Focus Malaysia

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.